If your online store accepts credit or debit card payments, you’re already bound by one of the most consequential security frameworks in global commerce — the Payment Card Industry Data Security Standard (PCI DSS). For eCommerce businesses in Singapore, this isn’t optional reading. It’s the difference between operating confidently and facing monthly fines, payment gateway suspensions, and data breach liability that can cost millions.

Here’s your complete, no-fluff guide to PCI DSS compliance — from understanding your merchant level to passing your first assessment.

What Is PCI DSS and Why Does It Apply to You?

PCI DSS is a globally recognised security standard created by the five major card brands — Visa, Mastercard, American Express, Discover, and JCB — to protect cardholder data across every transaction. Any business that stores, processes, or transmits payment card information must comply, regardless of size or geography.

In Singapore, the Monetary Authority of Singapore (MAS) explicitly references PCI DSS as a benchmark that financial institutions and payment processors should align with when handling cardholder data. If your eCommerce store accepts card payments through any gateway — Stripe, PayNow-linked services, Adyen, or a local acquirer — PCI DSS applies to you.

The current enforceable version is PCI DSS 4.0.1, which became fully effective on 1 April 2025. It introduces 51 new requirements focused on modern threats like Magecart attacks, browser skimming, and supply chain vulnerabilities — all highly relevant for online stores.

Understanding PCI Merchant Levels

Your compliance obligations are determined by your transaction volume. There are four merchant levels:

Level 1 applies to merchants processing more than 6 million card transactions per year. These businesses require an annual on-site audit by a Qualified Security Assessor (QSA) and a quarterly network vulnerability scan.

Level 2 applies to merchants processing 1 to 6 million transactions annually. They must complete an annual Self-Assessment Questionnaire (SAQ) and quarterly scans.

Level 3 covers merchants with 20,000 to 1 million eCommerce transactions per year — where most growing Singapore online stores land. An SAQ and quarterly scans are required.

Level 4 applies to merchants processing fewer than 20,000 eCommerce transactions annually. SAQ completion is typically required, and your acquiring bank may request quarterly scans.

The key takeaway: even as a small eCommerce operator in Singapore, you are not exempt. All levels are subject to the same core security requirements and potential penalties.

SAQ vs. Full Audit: Which Path Is Yours?

For most eCommerce merchants, the path to compliance runs through a Self-Assessment Questionnaire (SAQ) — a structured checklist that lets you evaluate your own environment against PCI DSS requirements.

There are multiple SAQ types. The most relevant for eCommerce firms are:

SAQ A is designed for merchants who fully outsource payment processing to a compliant third-party provider and never touch cardholder data directly (e.g., using Stripe Checkout or a fully redirected payment page). This is the simplest form, though PCI DSS 4.0.1 has added new controls to SAQ A around script management and page integrity monitoring.

SAQ A-EP applies to merchants with a partially outsourced eCommerce environment where their own web server hosts or influences the payment page. More controls apply here, particularly around web application security.

SAQ D is the most comprehensive form, required when merchants store, process, or transmit cardholder data themselves — essentially a full self-assessment covering all 12 PCI DSS requirements.

Level 1 merchants bypass the SAQ entirely and must undergo a formal Report on Compliance (ROC) conducted by a QSA. This is a rigorous, evidence-based audit that produces a binding compliance certification.

If you’re unsure which SAQ applies to your store, your acquiring bank or payment gateway provider is the authoritative source.

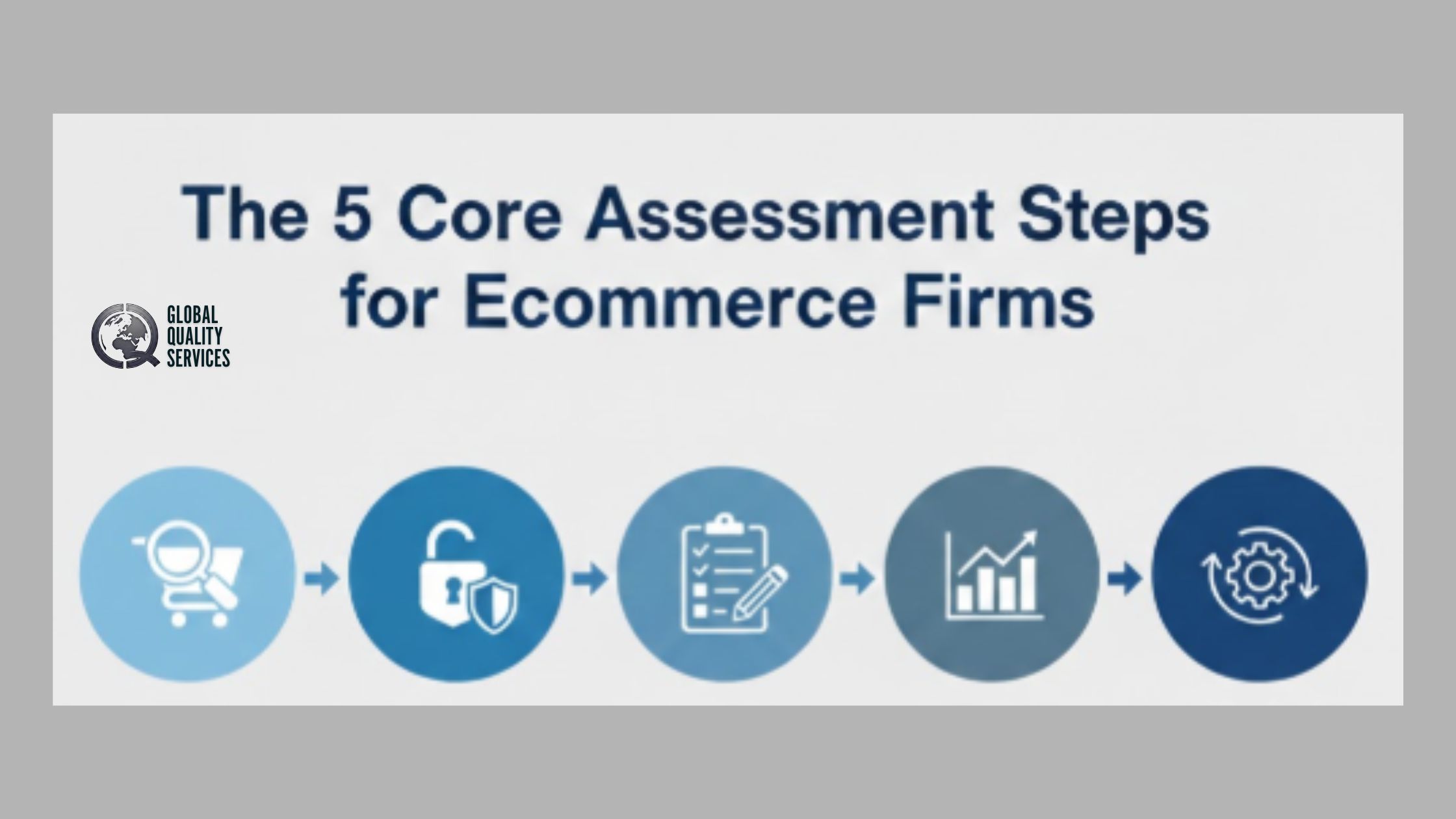

The 5 Core Assessment Steps for eCommerce Firms

Getting PCI compliant is a structured process. Here’s how most Singapore eCommerce businesses should approach it:

- 1. Define your Cardholder Data Environment (CDE). Map every system, application, and third-party integration that touches payment data. The smaller and more isolated your CDE, the simpler your compliance journey.

- 2. Conduct a gap assessment. Compare your current security posture against the 12 PCI DSS requirements. Focus areas for eCommerce include firewall configuration, encryption of data in transit, multi-factor authentication (MFA), and web application security.

- 3. Remediate identified gaps. Implement the missing controls — this could include deploying a Web Application Firewall (WAF), configuring TLS 1.2 or higher, enabling MFA for all admin access, and establishing a formal patch management process.

- 4. Complete your SAQ or engage a QSA. Depending on your level, either complete the appropriate SAQ honestly and thoroughly, or schedule a formal audit with an accredited QSA.

- 5. Submit your Attestation of Compliance (AOC). Once your SAQ or ROC is finalised, submit the AOC to your acquiring bank or payment facilitator as evidence of compliance.

Documentation: What You Must Keep on File

PCI DSS is not just a technical exercise — it’s heavily documentation-driven. Key records every eCommerce merchant must maintain include an annual scope definition document, network diagrams showing data flows, written information security policies, evidence of quarterly vulnerability scans, access control logs and user provisioning records, and incident response plans with training records. Under PCI DSS 4.0.1, you are also required to maintain an inventory of all payment page scripts and document monitoring of HTTP headers — a critical new control targeting Magecart-style attacks.

Penalties for Non-Compliance

Non-compliance with PCI DSS carries serious financial consequences. Monthly fines typically begin at $5,000 and can scale to $100,000 depending on the size of your business, transaction volume, and how long the violation persists. These penalties flow from card brands to your acquiring bank, which passes them on to you.

Beyond monthly fines, a data breach while non-compliant can trigger forensic investigation costs, card reissuance fees of $3–$10 per compromised card, increased interchange rates, and in severe cases, termination of your ability to accept card payments altogether. IBM’s 2024 Cost of a Data Breach Report puts the average total cost of a breach at $4.9 million globally — a figure that makes the cost of proactive compliance look very reasonable.

The Annual Renewal Cycle

PCI DSS compliance is not a one-time event — it’s an annual obligation. Every 12 months, you must re-complete your SAQ or ROC, conduct quarterly network vulnerability scans (typically four per year), review and update your scope documentation, and resubmit your AOC to your bank or payment facilitator. Changes to your payment environment — such as switching gateways, launching a new checkout flow, or adding a subscription billing engine — can change your SAQ type and may require an interim assessment.

Build compliance renewal into your annual security calendar, ideally 2–3 months before your AOC expiry date.

Ready to Get PCI Compliant?

Whether you’re a growing D2C brand or an established Singapore marketplace, the path to PCI DSS compliance is clear — it just requires the right guidance and the right tools. The most efficient approach is to minimise your CDE scope by using a fully hosted, PCI-compliant payment gateway, then layer your SAQ completion and quarterly scans on top.

Start your PCI DSS compliance journey today with Global Quality Services — map your cardholder data environment, identify your merchant level, and book a call with a Qualified Security Assessor who understands the Singapore eCommerce landscape.

FAQs

Q: Is PCI DSS legally required in Singapore?

PCI DSS is not a statute — it’s a contractual obligation enforced by card brands through your acquiring bank and payment gateway agreements. However, MAS references it as a security benchmark for financial institutions, and non-compliance can trigger commercial penalties and termination of card acceptance privileges.

Q: Does using Stripe or PayPal make me automatically PCI compliant?

Not entirely. Using a compliant gateway significantly reduces your scope, but your own website and server infrastructure may still be in scope — especially if your web server hosts redirect scripts or embedded payment iFrames. Under PCI DSS 4.0.1, Requirements 6.4.3 and 11.6.1 apply to many merchants using third-party payment pages.

Q: What is the difference between an SAQ and a ROC?

An SAQ (Self-Assessment Questionnaire) is completed by the merchant themselves to document their compliance status. A ROC (Report on Compliance) is produced by an independent Qualified Security Assessor following a formal audit. Level 1 merchants are required to obtain a ROC; other levels typically use the SAQ route.

Q: How often do I need to complete a vulnerability scan?

Quarterly — at minimum four times per year. Scans must be conducted by an Approved Scanning Vendor (ASV) accredited by the PCI Security Standards Council.

Q: Can a data breach happen even if I’m PCI compliant?

Yes, but the consequences are significantly reduced. Merchants who were fully compliant at the time of a breach typically face lower fines, reduced liability, and better outcomes with their acquiring bank and card brands than non-compliant merchants.

Q: What changed in PCI DSS 4.0.1 that affects eCommerce stores?

The most significant changes for eCommerce merchants are Requirements 6.4.3 (script inventory and authorisation management for all payment page scripts) and 11.6.1 (change and tamper detection for payment page HTTP headers and contents). These controls directly address Magecart and web skimming attacks — now fully enforceable as of 31 March 2025.